Slaying Crypto’s Mythical Beasts

As we wrap up 2022 and head into 2023, it’s time to toss the dross to allow us to lay down a strong foundation for the coming years. What better way to do this than to tackle some of the myths that surround digital assets? We address our choices for the top five and hope that this provides the proper framework for our readers to think about digital assets constructively.

5. Crypto is mainly used for illegal activities

“I think many (cryptocurrencies) are used, at least in a transaction sense, mainly for illicit financing."

- Janet Yellen, January 19, 2021

When such a statement is uttered by the current US Treasury Secretary and a previous Chair of the US Federal Reserve, this must be correct, right? The interesting feature about digital assets and the underlying blockchain technology is that the flow of transactions is transparent, and the accounts can be pseudonymously identified. Contrary to popular perception, there is no full anonymity on a blockchain! Chainalysis is a blockchain data platform that has taken advantage of this fact to build a strong reputation for on-chain analytics and tracking. According to their review of illicit crypto transactions through the end of 2021, although illicit use of crypto reached an estimated all time high of $14 B in 2021, this represents a mere 0.15% of all digital assets transactions volume for the year.

Source: Chainalysis

In contrast, in a FBI (US Federal Bureau of Investigations) statement to the Senate Banking, Housing, and Urban Affairs Committee back in late 2018, the Section Chief Steven D’Antuono stated “The U.N. Office on Drugs and Crimes estimates that annual illicit proceeds total more than $2 trillion globally, and proceeds of crime generated in the United States were estimated to total approximately $300 billion in 2010, or about two percent of the overall U.S. economy at the time.” Furthermore, “cash transactions are particularly vulnerable to money laundering. Cash is anonymous, fungible, and portable; it bears no record of its source, owner, or legitimacy; it is used and held around the world; and is difficult to trace once spent.”

How is it that a 2018 statement by the FBI is relying on reports from the UN back in 2010 when Chainalysis is able to publish in early 2022 the amount of illicit crypto activities through the end of 2021? If illicit crypto activities reached a peak of $14B in 2021, how much illicit activity was conducted in fiat cash? Are the features of cash – anonymous, bearing no records, and difficulty to trace – the same features found in digital assets? If it isn’t clear to the reader, these questions are meant to be rhetorical.

4. Bitcoin is a good inflation hedge

Hyperbole is used by both sides of the digital assets aisle, and the crypto community employed its share to promote the ownership of digital assets. Bitcoin’s capped token supply seems to readily parallel the limited supply of gold in circulation. However, neither digital assets nor gold serve as good inflation hedges, as we previously discussed here. To quickly summarize our points with a particular focus on BTC,

BTC is a long duration asset without cashflows. Rising inflation typically leads to rising rates, hurting all long duration assets. BTC is no exception.

Moreover for BTC, correlation is hard to assess for such a short history given that it is largely absent of inflation shocks. However, if BTC is expected to behave like digital gold, we will point out that gold too has a poor correlation with inflation to act as an effective hedge.

Investors who want a true inflation hedge should directly trade inflation swaps or TIPS. For retail investors who don’t have access to derivatives, a fixed-rate mortgage is a very good inflation hedge.

3. Bitcoin can be forked so it has an unlimited supply

Bitcoin’s, and most other digital assets for that matter, whitepaper and source code are all transparent and open-sourced. It is possible to fork (copy, modify, and deploy) Bitcoin’s code to bootstrap another cryptocurrency. Indeed, many have done so, with Bitcoin Cash and Bitcoin Satoshi Vision being a couple of the better-known forks. The concern is that forked assets can readily cannibalize each other’s and the original cryptocurrency’s utility and value. However, while it is easy to fork software code, it is far harder to fork social consensus. A forked platform would need to convince users to adopt another platform, that its applications are better, and that its platform for growth is superior to that of the original. The chart below shows the evolution of active addresses on Bitcoin versus Bitcoin Cash, a forked platform. That ratio has not grown since the middle of 2017 and arguably has declined from just over a year ago. The same can be said for Ethereum Classic and Ethereum-POW both of which remained but mere shadows of Ethereum.

Sources: coinmarketcap.com, bitinfocharts.com

2. Bitcoin mining is bad for the environment

The statistics don’t look pretty. Bitcoin mining’s energy usage has been equated to that similar of a smaller economy on par with Denmark or Finland.

Source: Cambridge Bitcoin Electricity Consumption Index

While this statement refers to only Bitcoin, many detractors sweep all of digital assets under the same rug. But this statement and its broader version for all digital assets are void of context. It presupposes that digital assets have no value. It ignores that the fact that there are alternative consensus mechanisms, such as Proof-of-Stake, that are far mor energy efficient. It puts the onus solely on crypto miners to be responsible for its mix of energy usage.

Ethereum is a prime case-study of how much energy is saved by migrating from a Proof-of-Work (PoW) consensus mechanism to a Proof-of-Stake (PoS). The chart below indicates that under the PoW consensus, Ethereum’s energy usage was comparable to that of Bitcoin. After The Merge, its energy consumption dropped over 99%. If we’re drawing analogies to countries, that’s dropping Ethereum’s usage from that of Finland’s to Gibraltar’s.

Source: EthereumEnergyConsumption.com

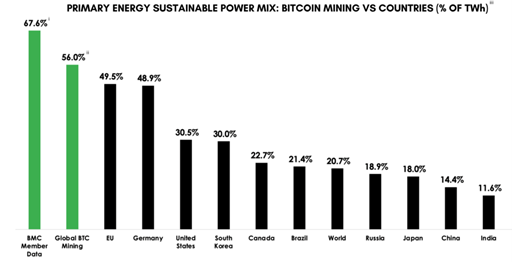

Quite importantly, if we were to hold Bitcoin miners to the task of being socially responsible when it comes to sourcing renewable energy, we see that this cohort is doing an admirable job. According to the Bitcoin Mining Council (BMC), bitcoin miners globally source 56% of their energy from sustainable sources and BMC members are even more impressively so at over 67%. This compares to the EU at 50%, US at 30%, and most countries with a far lower mix of sourcing sustainable energy sources.

Source: Bitcoin Mining Council, Q2, 2021

Finally, implicit in the statement that Bitcoin is bad for the environment is the unstated assumption that bitcoin, and other digital assets, have no real value. This leads to our number one myth.

1. Digital assets have no real use cases and no intrinsic value

Everything we do requires energy consumption. Our thinking requires food; designing, building, and maintaining a golf course requires diesel and electricity; transportation to support global trade require massive amounts of carbon-based and renewable energy sources. As we become more environmentally conscious, we are rightly asking how we can develop and utilize more sustainable energy sources. However, unlike digital assets, hardly anyone is using energy consumption as an argument to ban these activities. This is an implicit nod that these products and services provide value to its users; in contrast, digital assets don’t.

Cryptocurrencies have demonstrated that it can be used for a social good. According to Chainalysis’s 2022 Global Crypto Adoption Index report, the top 10 adopters were Vietnam, Philippines, Ukraine, India, US, Pakistan, Brazil, Thailand, Russia, and China. Why are so many in the top 10 among the lower income emerging economies? Chainalysis cites that these economies “often rely on cryptocurrency to send remittances, preserve their savings in times of fiat currency volatility, and fulfill other financial needs unique to their economies.” Anecdotally, according to a New York magazine article, “ crypto has become one of the only ways to reliably send money in and out of Afghanistan, its banks stuck in a perpetually sanctioned, purgatorial state. Increasingly, NGOs rely on it as a means of delivering aid and are conducting pilot programs to test its reliability.” In a separate article from the Center for Strategic & International Studies, crypto assets are currently aiding Ukraine in its defense from Russia with “ most donations [coming] from individuals around the world. As of March 9, the Ukrainian government claimed to have raised nearly $100 million from crypto donations. The crypto donations allow Kyiv to obtain funding instantly and are faster than soliciting donations settled through traditional financial channels.” To say or imply digital assets have no use cases or no intrinsic value is patently false.

Admittedly, the intrinsic value of a digital asset is hard to estimate. Market prices reflect the marginal trader and can at times be quite divorced from value. Metcalfe’s law, a valuation method premised on value being proportional to the number of peer-to-peer transactions in a network, appears promising although our analysis indicates that it is incomplete and needs to be augmented with analysis of bubble dynamics and better metrics of active addresses.

New myths will continue to bubble up around digital assets as old ones get popped. But this asset class underpinned by a new technology offers unprecedented transparency for us to investigate, trace, and verify. It’s our collective responsibility to ask the right questions and seek the right answers to move the developments forward in a balanced manner.